Buying a home: Do you really need 20% down?

There’s a widespread perception

that you need to put at least 20

percent down to buy a home.

Fortunately for home buyers that’s

just not true.

In fact, even in today’s mortgage

market, it’s still possible to buy a

home with a down payment of five

percent or less. You can even get a

mortgage with zero percent down

through certain programs, which

aren’t as hard to qualify for as you

might think.

RURAL DEVELOPMENT –

A ZERO DOWN OPTION

You can get a zero-down

payment mortgage through the

USDA Rural Development. There

are income restrictions; a family of

four or less can earn no more than

$74,750 and a family of five or more

can earn as much as $98,650.

USDA’s definition of rural is quite

broad and includes the city of

Yankton and all of the communities

in the Yankton market.

VA – ANOTHER ZERO

DOWN OPTION

You typically have to have served

or be serving in the military in order

20 n TODAY’S HOME – SPRING 2013

to qualify for this option.

FHA DOWN PAYMENT

AS LOW AS 3.5%

This program allows you to

obtain a mortgage with a low down

payment if you are not eligible for a

Rural Development or a VA loan.

CONVENTIONAL MORTGAGES

These programs require as little as

three percent down.

RATE LOCKS

What are mortgage rate locks and

how do they work? They are a

written promise by a lender to offer a

certain interest rate for a specific

length of time, usually 60 days or

less. The rate lock doesn’t just

guarantee the interest rate, but also

specifies other aspects of the loan,

i.e., the term of the loan, the down

payment, etc. Options to lock for a

timeframe longer than 60 days are

available but additional fees or higher

rates may apply. You also have the

option to “float” your interest rate. If

you think that interest rates will drop

prior to the closing of your mortgage

loan you may want to consider

“floating” your rate rather than

locking your rate.

CREDIT SCORES –

WHAT AFFECTS YOUR

CREDIT SCORE

Credit scores are very important

in the mortgage loan approval

process. Making your monthly

payments on time is a very important

factor in the scoring process but there

are additional factors that can impact

your score. You need to know what

these factors are and what you can

do to improve your score. At First

National Bank South Dakota we can

provide you with helpful information

to improve your scores.

The credit score is based

on five factors:

1. Payment history affects 35% of

your credit score. Paying on time can

mean the difference between an

average and an exceptional score.

2. Amount borrowed compared

to your available credit affects 30%

of your score. Ideally you want to

borrow less than 33% of your

available balances. It is better to owe

a smaller amount on several cards

than to max one card to its limit.

3. Length of credit history

comprises about 15% of your score.

Avoid opening new credit cards

because the lender is offering an

initial low interest rate.

4. Inquiries and new debt

accounts for about 10% of your

score.

5. Type of debt accounts for

approximately 10% of your score.

Installment debt, such as a car loan,

is looked upon more favorably than

revolving debt such as a credit card.

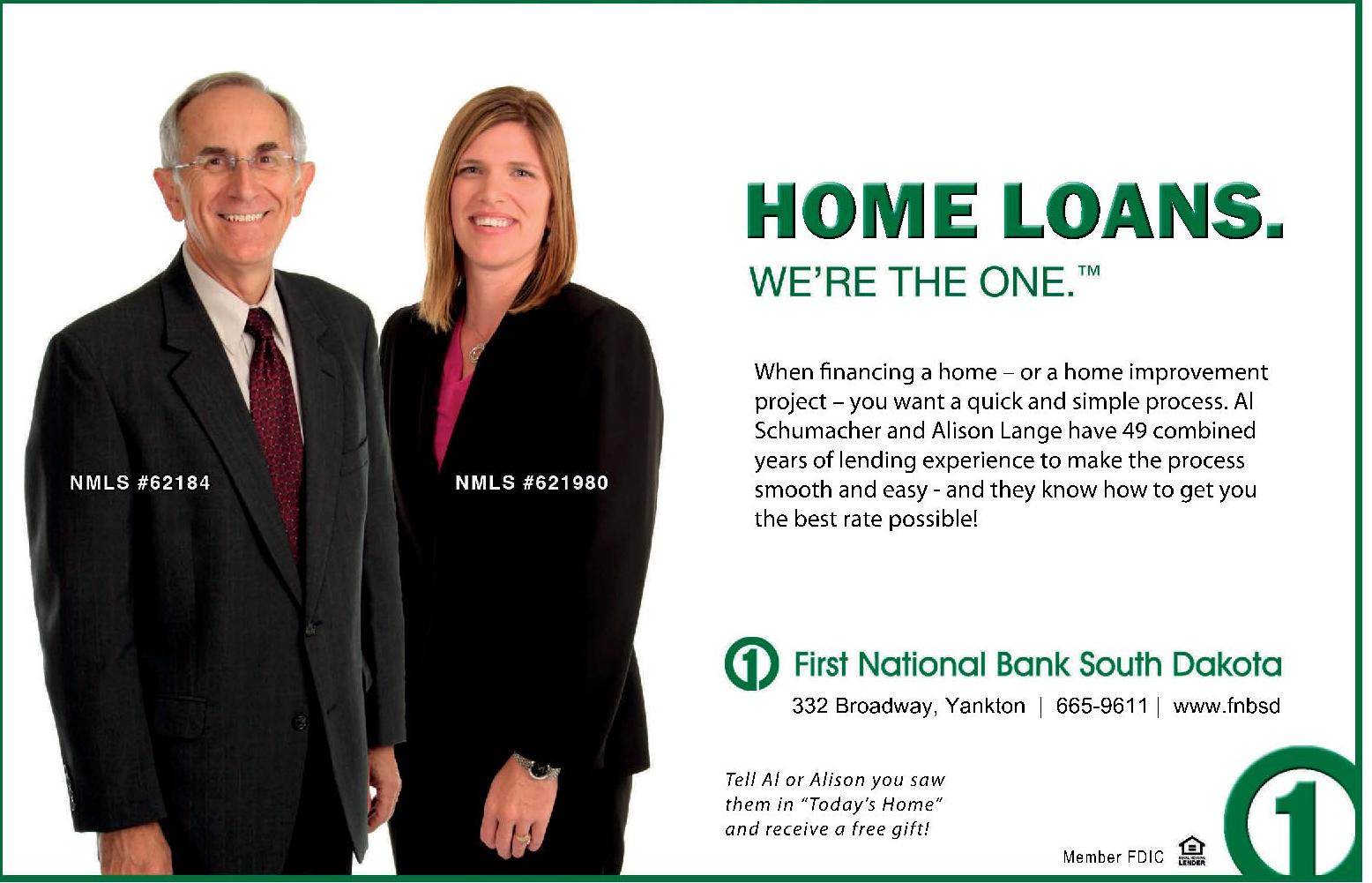

Which Mortgage Option is Right for

You?

Obtaining a mortgage loan can be

confusing with all the various types

of financing available. In addition,

credit scores play a much greater role

in today’s financing than they have in

past years. To assist you in obtaining

the mortgage loan that is right for

you, contact Al Schumacher or

Alison Lange at First National Bank

South Dakota, 665-9611. They will

discuss the options available and

which best fit your needs. With 49

years of combined lending experience

they can assist you and make the

process smooth and easy.

n Editorial provided

by First National Bank South Dakota

Previous Page

Previous Page